IVGID Forensic Audit Report Released: What Property Owners Need to Know

Why are you paying a $1,375 Recreation Fee in 2025 on your property tax bill?

Newly published book Tahoe Illusions https://www.amazon.com/dp/B0FMG7J9G9 documents the 57-year fraud behind IVGID’s special assessment tax, why it should have ended years ago, and why FBI, state agencies, and your elected officials won’t stop the collection. Every property owner needs to read this.

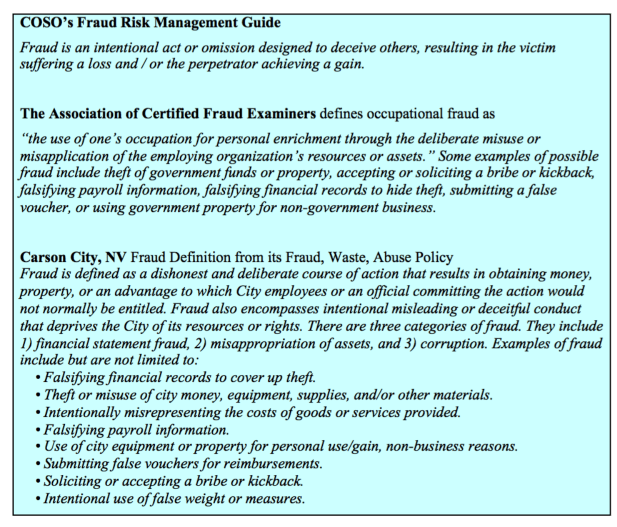

“The scope of the audit was to identify fraud risk, it was not to identify fraud.”

IVGID Trustee Ray Tulloch, August 7, 2024, Committee meeting on Local Government Finance – State of Nevada Tax Department

And that is why the report doesn’t include the word F-R-A-U-D. Because Trustee Tulloch and General Manager Bobby Magee made sure FRAUD was not in SCOPE. This was a BAIT-AND-SWITCH as the original audit scope in the RFP was clear.

***

The long-awaited and carefully worded forensic audit report for the Incline Village General Improvement District (IVGID) has been released, revealing significant concerns about the district’s financial management and internal controls. As property owners and stakeholders in IVGID, it’s crucial to understand the implications of this report and take appropriate action.

Key Findings

The report identifies a high risk of fraud and abuse within IVGID’s control environment, citing numerous internal control weaknesses. These issues span from transactional-level problems to deficiencies in the review and monitoring processes of internal controls. Specific concerns include:

1. Weak disbursement processes, with instances of no approver or self-approval

2. Insufficient support for vendor disbursements

3. Bank reconciliations not performed for multiple accounts

4. A failed implementation of a new accounting system

5. A “loose culture” around financial controls

6. High employee turnover

7. No physical inventory for fixed assets, food & beverage operations, and retail shops for 3 years

The audit categorized 41 observations, with 16 ranked as high risk, 12 as moderate risk, and 13 as low risk. This distribution suggests that the issues are serious and pervasive throughout the organization.

Report Leaves Questions Unanswered

An unreconciled difference of over $7 million dollars existed as of June 2023 in IVGID’s main checking account. The reason? The report does not say.

Personal use of procurement cards was found. What did these employees buy? How much money was involved? And were the employees disciplined? The report is silent. And the report is not clear on the number of pcard transactions that were examined, so it is unknown whether other uses of pcards for personal use occurred.

The report fails to quantify amounts or provide details for multiple high risk observations. As RubinBrown was paid around $400,000 for the report, the question of less than adequate work by RubinBrown should be followed up by Trustee Tulloch, as he was the Board point of contact.

The report does not state that the general ledger is still out-of-balance. In our review, the general ledger is now ($15,782,015.80) out-of-balance; for fiscal year 2023, it was $5.3 million out-of-balance. Yet, hundreds of thousands of dollars were paid to BakerTilly for temporary accounting services. IVGID’s Finance Dept / Adam Cripps cannot explain what is wrong or how it will be corrected.

The Federal Government Defines Personal Use of Procurement Cards as Fraud

The forensic audit report should have stated that fraud was found, even though the employee reimbursed IVGID. Here’s why:

- Definition of fraud: The Office of Management and Budget (OMB) Circular A-123 defines fraudulent purchases as those “made by cardholders that were unauthorized and intended for personal use”. This definition applies regardless of whether reimbursement occurs later.

- Personal use is prohibited: Using government procurement cards for personal purchases is against IVGID policy and potentially illegal, even if there’s an intent to reimburse.

- Reimbursement doesn’t negate fraud: The fact that the employee reimbursed IVGID does not change the fraudulent nature of the initial transaction. Fraud occurs at the time of the unauthorized personal purchase.

- Multiple instances: There were two instances of personal use by one individual, which suggests a pattern rather than an isolated mistake.

- Criminal implications: Personal use of institutional funds, including procurement cards, may be construed as a criminal act, regardless of reimbursement. “Wire Fraud” can be used to prosecute for personal use of a credit card such as this case when a hospital employee used a hospital credit card for personal use. And here is a case where a water district employee was charged with wire fraud for using the district’s credit card and checks to pay for personal expenses.

LAND Account Not Examined

The LAND account, which we found to have over 13 million dollars in improper capitalized expenses was NOT examined. Three forensic firm partners were provided with this information, as well as the IVGID Audit Committee. This leads us to have concerns that other seemingly fraudulent activity may have been purposely excluded.

It is surprising that the report says:, “We recommend IVGID research the Federal and State of Nevada tax regulations to assess whether or not the employee clothing allowance should be employee taxable income.” Doesn’t the forensic auditor, Rubin Brown, KNOW the specific Federal IRS rules for employee uniforms and that Nevada has NO state income tax? This issue was also part of the information provided the forensic audit partners.

What This Means for Property Owners

These findings indicate potential mismanagement of public funds and resources. As property owners, you have a vested interest in ensuring that IVGID operates efficiently and transparently, as its performance directly affects your property values and quality of life in the community. Recommended Actions for Property Owners:

1. Stay Informed: DOWNLOAD and read the full forensic audit report. Consider attending upcoming IVGID Board meetings where the findings will be discussed. You can attend meetings virtually.

2. Demand Accountability: Contact your IVGID Board Trustees and express your concerns. Insist on a clear, time-bound action plan to address the issues identified in the report. Ask them why the LAND account was not addressed. And ask them whether they will request law enforcement to investigate.

3. Support Reforms: Advocate for the implementation of stronger internal controls, improved financial reporting processes, and enhanced transparency in IVGID’s operations.

4. Monitor Progress: Keep track of IVGID’s efforts to address the audit findings. Request regular updates from the Board on the implementation of corrective measures.

5. Consider Legal Action: If you believe that IVGID’s management has been negligent or engaged in misconduct, consult with legal professionals about potential actions that property owners could take collectively.

6. Support Independent Oversight: Advocate for the establishment or strengthening of independent oversight mechanisms to ensure ongoing monitoring of IVGID’s financial management. Currenly, the Nevada Department of Taxation is supposed to provide oversight – but it is a rubber stamp. Consider contacting the Washoe County Commissioners and your elected representatives in the Nevada legislature.

The release of this forensic audit report indicates all is not right at IVGID. Only by taking an active role in demanding accountability and supporting necessary reforms, will changes be made. Remember, your engagement and vigilance are crucial in safeguarding the long-term interests of the Incline Village/Crystal Bay community.

The forensic audit report was released to the public at 9:25 AM PDT on July 10, 2024, less than 9 hours before the IVGID Board meeting in which it was to be discussed. Therefore, the public did not have sufficient time to be aware that the report would be on the agenda, and to read its contents. The timing shows NOTHING HAS CHANGED AT IVGID WITH THIS REPORT.

IVGID Mgmt Response to the Rubin Brown Report [updated July 24, 2024] For many of the observations/findings, the response is “more to come in the weeks ahead.” For most audits, this response would be viewed as inadequate, as it is a deferral and not a response with a specific action plan for the observation/finding. Read the AI (artificial intelligence) analysis of the IVGID management response.

- (updated 7-31-2024 with Chris Nolet’s public comments)

Comments by former Chair of the Audit Committee, Chris Nolet, at the July 31, 2024 Board Meeting

Chris Nolet, full time resident, former chair of the [IVGID] Audit committee through February of [2024] 24. I want to comment on the Rubin Brown fraud report tonight.

One of the major problems with the report that we raised during the scoping process when I was following the audit committee is they never defined fraud, but yet they concluded they didn’t see any.

Well, that’s utterly ridiculous.

So they identified 16 areas of high risk of potential fraud and abuse.

That’s staggering.

And they said there was no tone at the top with regard to leadership to mitigate these risks.

That more than validates what some of us said last summer.

And for anyone, including [resident] Mick Holman, to say that a $7 million difference between book and the bank recs [reconciliations] is not fraud is utterly unconscionable.

CAPEX [Capital expenditures], as Mr. Dobler has been saying for years, unable to reconcile the ledger to the general ledger.

Mick last year said I was spreading hysteria. The findings from this report are much worse than I ever suggested. So Mick, I accept your apology.

With these findings, there’s likely no [2024] 24 audit.

As I suggested a couple [of ] meetings ago, there’s likely no [2023] 23 audit being completed.

And any of these assertions I’m making tonight, if I’m wrong, please correct me and I’ll be happy to correct my public comments in the future.

As I explained during two tutorials last year, the fraud definition that everyone should have been working with was statement of auditing standards number 99, auditor’s consideration of fraud and financial statement audit.

Of course, these results represent fraud under that standard and Michaela [IVGID Board Trustee Tonking] can validate that at some future date with you on a private session.

But to say, [chuckling] as many have said, that, well, there’s a lot of risk of fraud, but there isn’t any fraud is utterly ridiculous.

I also like to point out that in February of [2024] 24, I suggested very strongly in a very difficult phone

call with some of the board members, at least one that, you know, promoting Bobby [Magee] to GM [General Manager] and promoting Adam Cripps to acting DoF [Dept of Finance] was going to result in both of them failing, which here we are, they have.

I don’t know where Adam is, maybe he’s on an LoA [Leave of Absence], but certainly the zero based budgeting process was a debacle, to say the least.

In conclusion, I said on March 28, 2024, there will be no. [2023] 23 audit and likely no. [2024] 24 audit.

So please work with Jennifer Farr, squeeze this conclusion out of her and save your money.

And as far as the management rebuttal went, completely unacceptable. It wasn’t vetted with the general manager.

And I’ll just point out lastly, [TIME BUZZER]because I won’t point out lastly, thank you.

Chris Nolet is a retired CPA and former EY partner.

We definitely need an Oversight Committee

Not a bad idea – but an Oversight Committee might not be enough. The Nevada Dept of Taxations Committee on Local Government Finance IS the Oversight Committee for General Improvement Districts in Nevada.

The 10 members just hold meetings and do nothing. And most are CPAs licensed in Nevada.

If there are no consequences, and no one is held accountable, nothing will change.

The results of the Forensic Audit is not surprising to me. For years folks like me, and certainly others, have known that IVGID has been incompetent. What is currently depressing is that some of us thought that a majority Board of Sara, Matt and Ray would see the ship alright, but that did not happen. Those three individuals have been as incompetent as former Trustees like Callicrate, Wong, etc. It is unfortunate, but our Trustees past and present are worthless, and they are definitely part of the problem.

I suspect this will not occur since a lot of our property owners support the stupidity of our Trustees, but the Administration of IVGID needs to move to the Department of Taxation (Our Trustees are idiots, and I suspect The Department of Taxation is no better (DOT), but it’s quite apparent IVGID, as managed, is totally incompetent).

I hope someone with better legal skills than I can devise a solution where property owners like me can refuse to pay the Rec Fee because of the incompetence, and stupidity, of IVGID.

Elect Frank Wright, he has been exposing the mismanagement for 15 years. But the residents just didn’t believe things could be this bad, well surprise! It’s your community!

This report and findings is highly disturbing. As an Incline Village full-time resident, I DEMAND accountability and answers. There are red flags all over the place in this report. The report is clearly insufficient and has failed to fully investigation the improper use of funds by various parties. I think legal intervention is required to investigate potential fraud and to charge individuals with theft where applicable. This demonstrates how much of IVGID is a complete shit show.

An investigation by law enforcement is clearly needed. If the Trustees are unwilling to request such an investigation, what does it say about them?

The results to me are not surprising. This is a “government” entity–not a private for-profit endeavor. None of the individuals working for IVGID have skin in the game. Its just a job. Employee turnover speaks loudly. You get what you pay for (usually). If you want a well-run ship, a professional tightly controlled and legally compliant organization, you need to hire (and pay) an experienced CEO, CFO, HR exec, and CLO, and give them the budget they need, and let them put in place the proper systems and controls organizationally. That’s not happening at IVGID. There’s no stomach to pay for that. So you get what you got. A mostly well meaning effort composed of mostly good people doing the best they can, to whatever level of competence they have, and accessing the level of resources provided to them.

Respectfully disagree. The pay scales of management are extremely high. Property owners are not getting what they’re paying for. IVGID has over 830 employees, about 144 are full-time. No, this is a cultural problem. The Fraud Triangle: Opportunity, Motivation, and Rationalization.

IVGID financials have been a long-standing mess for many years, going back to GMs Horn and Pinkerton and Trustees Callicrate and Wong, more recently. It’s too bad Callicrate and Wong set it up for Winquest to be the fall guy to continue to mishandle and ignore the problems, while they did nothing to pursue rectifying IVGID’s financials. No wonder he refused his performance review once Callicrate and Wong neatly exited their Trustee seats. He knew what he was in for. But Winquest was underqualified for the GM role anyway so it worked out and he’s a Parks and Rec leader again.

We’ll see what the current Trustees do as next steps to address this mess, or will they punt it to the next Board as Callicrate and Wong did? Unfortunately Jaczecki and Tonking lack experience and courage to deal with these types of matters, seeing as they are beholden to IVGID employees and popularity with them and the golfing clubs. Homan might have the courage unless he’s swayed by the likes of the Schmitz and Dent-haters in the community. Wright would absolutely push for an investigation. There’s too little information about Swenson and Case at this point to know how they might act.

The financial statement presentation format is beyond horrible and there isn’t much revenue or expense detail.

Most stunning at the moment is the fact that $400,000 was paid to Rubin Brown for an incomplete and inadequate report!

Now why would Trustee Tulloch, who was the point of contact for the Board as he is Treasurer, allow Rubin Brown to deliver an incomplete and inadequate report? By spending $400,000, he can say there is no more budget. And the report does not single out any employees – even though procurement card fraud was found.

An investigation by law enforcement is needed.IVGID has demonstrated it cannot investigate itself.

IVGID has been run like a private club not a professional organization for decades. Strong internal financial controls should have been established when IVGID was created. We will never really know the full extent of financial mismanagement especially with a flawed forensic audit.

It’s long past time for residents to demand a complete restructuring of the IVGID organizational chart and a thorough analysis of every position and every expense. Go back to zero based budgeting, put in place the necessary accounting and financial controls and make sure that bank statements are reconciled in a timely fashion every month. This just scratches the surface of what needs to be done to fix things.

I am a CPA with almost 47 years of experience and have audit and governmental accounting experience including A-133 audits and would be happy to assist at some level, as I own a home in Incline village and find this discussion to be somewhat comical, but serious as to the magnitude of the dollars…and the issues presented.. a one time use of a Company credit doesn’t constitute fraud in most instances..and lacking controls leads to fraud..

If you read the forensic report, an employee used their procurement card for personal use more than one time. There is a link to the report in the article; for clarity, here is the link: http://ourivcbvoice.com/wp-content/uploads/2024/07/2024-0710_BOT_Supplemental_Material_ItemG1_IVGID_Forensic_Draft_7.9.24.pdf

I am sure your background and experience would be valuable – but do not be surprised if no Trustee contacts you. Several CPAs who live in Incline have volunteered their services – and neither management or the Trustees ever contacted them. Even a retired employee from Bechtel who had deep procurement expertise volunteered to improve their procurement processes; General Manager Bill Horn refused that offer.

Soo…We feel we’ve confessed the mess! now we sweep it under the rug & feel better.?

Nothing deep in the core of IVGID’s history has changed. The organization has a history-long track record of what it is now. Nothing short of shutting it down and restructuring it will change its course. Good luck.

I think you’re a little excited about the purchasing card items.

I carry a corporate card and personal cards. More than once, I have accidentally charged items intended as personal on the corporate card (this is really easy to do with Uber and things like DoorDash, especially if the numbers are very similar…and on business trips you use a lot of Uber and DoorDash).

This happens ALL THE TIME at my workplace- enough where we have a process to reimburse the company, management approval etc. It happens. It’s a mistake, it’s not fraud. If I did it more than once, is that a pattern?

The fact that there is some ridiculous OMB circular for the feds saying that charging personal expenses (accidentally) on a corporate card / purchasing card is FRAUD (clutching pearls) doesn’t mean we should go into a criminal process with our employees, PARTICULARLY when we aren’t an employer of choice. Mistakes happen, and when people reimburse the funds, the mistakes are corrected.

If someone does the same thing repeatedly in a high dollar value, sure, that’s a disciplinary issue. But I haven’t seen that evidence in this audit.

Your comment is an example of rationalization: “a way of describing, interpreting, or explaining something (such as bad behavior) that makes it seem proper, more attractive.” (Merriam-Webster dictionary).

Rationalization is one of the three components of the fraud triangle:

A corporate card is different than a procurement card.

For some history. In 2015. I and Linda Newman begin writing several memos to the Board of Trustees about improper accounting. None were ever addressed by the Board or Management of IVGID. One example would be the over payment of fees to PICA, a pipeline investigator. I wrote a report which was then review and studied by Trustee Schmitz and we concluded that about $200,000 to $300,000 was paid to PICA for work not performed. In February 7, 2020, I wrote a extensive memo about the investigation. Nothing was done and no response from the Board was received. During the past 5 years, prior period adjustments were required for errors in previous years. In addition, the auditors claimed that a serious deficiency existed in internal controls. During my two years on the audit committee, the committee addressed several flaws in the financial statements but received resistance from management. They did what they wanted. In the past three years, I provided 30 memos on irregular accounting to the Audit Committee. Actions should have been taken on 21 items (never done) and 9 still remained unanswered. No report and no action was taken by committee members as a revolving door of members existed.The nine issues were never resolved. Lastly one former audit committee member (who resigned) had extensive experience with software conversions and was willing to assist but the offer was ignored. As such almost three years have passed and the conversion remains incomplete.

These are just a few of the accounting and reporting death march. The trustees can only set policies and management should follow the policies. This is not done. The Trustees have a obligation to contact the county and the state and explain that the IVGID board cannot function properly for a going concern.

So based on Chris Nolet’s 7-31-2024 comments, Mr. Magee and Mr. Tulloch, the points of contact on the forensic audit, engineered no definition of fraud. The failure to reach an agreement on the definition of fraud for a forensic audit is an extremely serious deficiency. Here’s why:

1. Fundamental flaw: A clear definition of fraud is foundational to any forensic audit. Without it, the entire process is compromised.

2. Missed opportunities: By not using established definitions like those in Auditing Standard 99 or federal regulations on procurement card fraud, the auditors may have overlooked crucial instances of misconduct.

3. Limited scope: This omission likely resulted in a narrower investigation scope, potentially missing fraudulent activities that don’t fit whatever limited definition was used.

4. Reduced credibility: The lack of a agreed-upon fraud definition undermines the credibility and usefulness of the entire audit report.

5. Potential bias: It raises questions about whether there was an attempt to limit the audit’s findings by constraining the definition of fraud.

EXTERNAL INVESTIGATION BY LAW ENFORCEMENT NEEDED. Residents should file complaints with the Nevada Attorney General and the Washoe County Sheri’ff’s Office. The FBI? They have huge problems of their own that are bigger than IVGID.